Last Updated on May 22, 2026

If you are investing or owning a leaseback property in France as a non-resident, there are specific tax regulations and obligations that we will explain in this guide.

Leaseback property is a unique scheme in France, which is becoming even more popular.

What are the advantages and disadvantages of having a leaseback property? What exactly is a leaseback and how does it work?

If you are looking for a hassle-free investment in property in France, especially in tourist destinations, buying a leaseback may be right for you. In this guide, you will find everything you need to know.

What is a leaseback property?

A leaseback is an arrangement in which the company / tradesperson that sells the property, can lease back the same real estate from the purchaser.

In this situation, the company / business owner can continue to use the property, but no longer owns it. In the transaction, the seller becomes the lessee and the purchaser becomes the lessor.

A leaseback property transaction is the purchase of a freehold furnished property in a serviced residential building. Buyers own the freehold of the property, which is then leased back to a management company for a period of 20 years.

Who needs leaseback?

Companies use leaseback when they want to use the money invested in a property for other business goals, but want to use the same property to operate their business.

In this situation, the company can get both the property it needs to operate its business and the money from its sale.

Also, people who want to invest their money in a property and have a guaranteed annual income without any hassle of renting and managing it, with an option to use it for their own holiday.

What is the difference between a leaseback and a furnished rental property?

The main difference between rent and lease is their continuance. A rental agreement covers a period that is not explicitly specified, while a lease is valid for a period that is stated in the agreement. This lease lasts for 9, 11 or 12 years.

The lease is usually long-term, while rent is for short-term periods. The tenant pays rent to the landlord, while the lessee pays lease rentals to the lessor.

Buyers of leaseback are entitled to a refund of the 20% VAT due to a property purchase or taxes due when selling French property.

The owner is guaranteed a rental income from their property, which is usually 2-5% of the property’s value, adjusted annually for inflation according to rental indexes published by INSEE (National Institute of Statistics).

The property is managed by a management company that takes care of the rental and general maintenance of the property, so the owner doesn’t need to worry about it.

What is the French leaseback property scheme?

The leaseback scheme also referred to in some cases as “résidences de tourisme classées”, was introduced by the French government in 1967.

To a certain extent, it was designed for those who were seeking investment and a holiday shelter for a few weeks each year.

Those properties are usually located in desired tourist/rural areas such as beach or ski resorts, where accommodation is in high demand.

Leaseback and tax advantages in France

Leaseback of real estate in France has been popular in the last 30 years and there are serious tax advantages.

Buyers are entitled to a refund of the 20% VAT paid on the price of the purchase. This is making the purchase considerably cheaper.

All property owners are required to pay taxe foncière and this is still payable by the buyer.

Owners of leaseback properties are not paying Taxe d’ Habitation and Cotisation Foncières des Entreprises (CFE) in France – these local taxes are paid by the management company.

For the seller-lessee, the sale-leaseback may provide a tax benefit, because the deduction for rental payments may be greater than depreciation and interest deductions from interest financing.

Will I have to pay tax on my rental income in France?

Yes, even though the mortgage interest can be offset against the income.

This depends on the amount of rental income and expenses for the relevant tax year.

Even if there is a loss and no rental income tax is due for the current year, you are obliged to file French tax returns (Business and Personal income tax returns).

Income tax for non-residents and residents in France

The rental income is liable to tax in the country where the property is situated. You are liable for income tax on French rental earnings and it does not matter if you are a resident in France or not.

This means that even if you are a non-resident, you will need to submit the yearly tax return to the French authorities of your rental income in France (in addition to any French-sourced income).

You will also need to declare the income to the tax authorities in your own country. France has double-taxation agreements, which means that you won’t be taxed twice on the same income if you are a resident of the UK or Ireland.

The rate remains 20% for income up to €27,519. The tax is 30% for rental income beyond this level. The rates apply to the net rental income.

The date for submitting your personal non-resident tax return in France is 26th May.

The french tax return for non residents deadline is 19th May.

If you are a French resident, the rental income is added to your other income and taxed at a progressive rate (up to 45%).

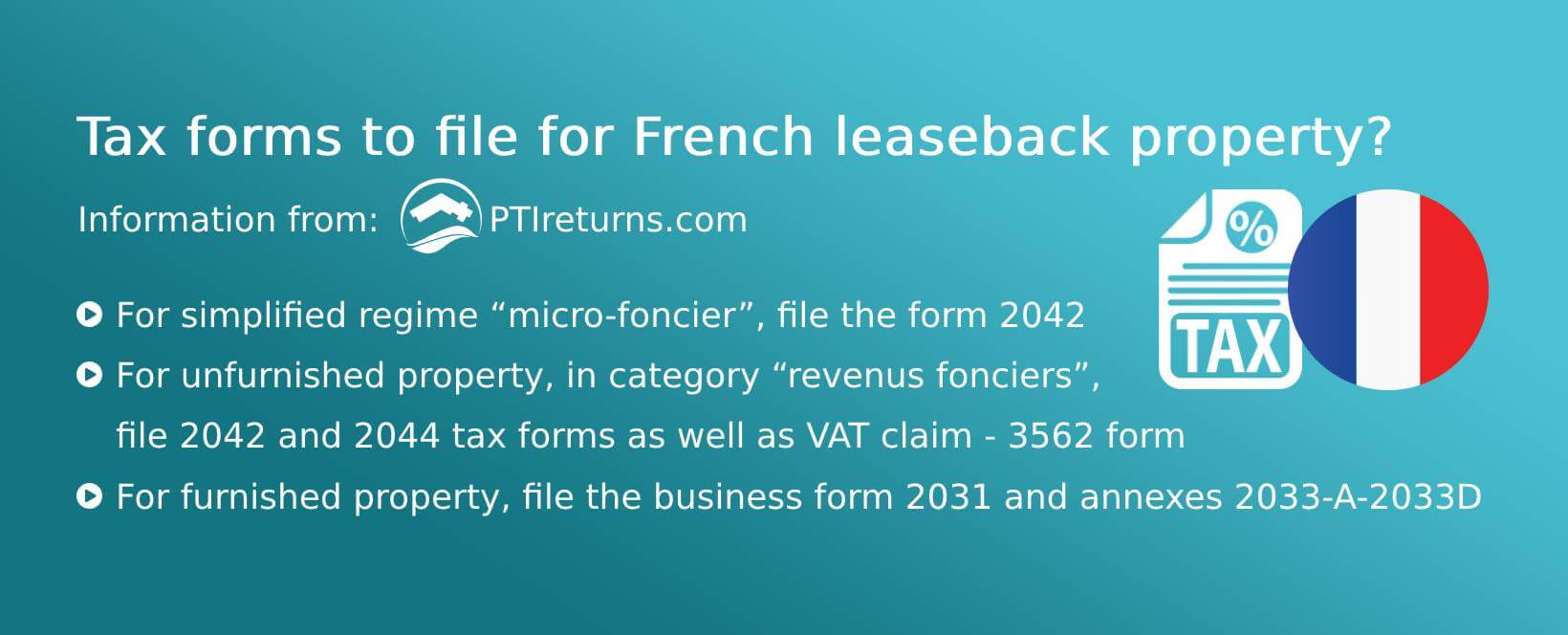

What forms should I file for my French property?

– If your rental income is taxed in the category of property income (“revenus fonciers”) under the simplified regime of “micro-foncier”, then you just have to file the tax form 2042.

– If your leaseback property is unfurnished, and your rental income is in the category of “revenus fonciers”, then you have to file 2042 and 2044 tax forms as well as VAT claim – 3562 form if you have paid VAT on expenses.

– If your leaseback property is furnished, then your rental income is in the category of the Business income – Bénéfices industriels and commerciaux (BIC). You have to file the business form 2031 and the annexes 2033-A-2033D, and the personal tax returns – forms 2042, and 2042 CPro.

Can I file my French tax return online?

It is obligatory that business tax returns should be filed online.

That is why you need to create a business online account (Espace Professionnel) on the French tax office website, using your number SIREN, and a valid e-mail address.

You can file your personal tax return online too. To create your personal online account (Espace Particulier) you need to have the following 3 tax identification numbers (or if you have already created your online account):

- French tax identification number: This 13-digit number is located on the top of the first page of your last tax return (“déclaration de revenus“) or on your last tax bill (“avis d’imposition“).

- Numéro de télé-déclarant: This 7-digit number is located on the top of the first page of your last tax return (“déclaration de revenus“).

- Revenu fiscal de référence: this number is located on your last tax bill (“avis d’imposition“).

To create your online account, you need to type in your 3 tax identification numbers and follow the procedure on this website: Mon compte fiscal en ligne.

I still need help with my French tax return. Who can assist me?

The French tax system is really complicated, but help is at hand.

(Property Tax International) PTI Returns offers a variety of tax return services. Our tax experts will assist you with the entire process of filing tax forms in respect of rental income.

PTI Returns can also create a personal or business account on the French tax office website instead of you.

Tax experts will keep you updated throughout the entire process and communicate directly with the French tax office on your behalf.

Need help? Then don’t hesitate!